{kind=link}

New York-area construction starts took a nosedive in March, as compared with a year ago, the Long Island Business News (LIBN) has reported, quoting regional Dodge Data and Analytics data.

However, Dodge reports that, nationally, new construction starts in March increased five percent to a seasonally adjusted annual rate of $743.7 billion, marking the third straight monthly gain.

This contrasts with the regional data for New York City, northern New Jersey, Hudson, Putnam, Rockland, Nassau, Suffolk, and Westchester counties and parts of Pennsylvania.

While there were more than $2.15 billion in construction starts in the New York area in March, these numbers were down 43 percent from the $3.75 billion in construction starts recorded in March 2016, according to Dodge Data & Analytics.

Both residential construction starts and nonresidential starts declined, LIBN reported, citing Dodge data. There was $951 million in nonresidential construction starts in March, 45 percent less than the $1.74 billion in starts a year ago. There was $1.2 billion in residential building starts in March 2017, down 40 percent from the $2.01 billion in starts recorded a year ago.

For the first three months of the year, total building starts are up 19 percent, going from $9.99 billion last year to $11.89 billion in the first quarter of this year.

Nonresidential construction covers office, retail, hotels, warehouses, manufacturing, schools, healthcare, religious, government, recreational, and other buildings. Nonresidential construction also includes streets and highways, bridges, dams and reservoirs, river and harbor developments, sewage and water supply systems, missile and space facilities, power utilities and communication systems.

Single-family and multifamily housing are considered residential buildings.

Nationally, the total construction growth in March was led by the nonbuilding construction sector, and particularly by public works which featured the start of two large pipeline projects – the $4.2 billion Rover natural gas pipeline in Ohio and Michigan, and the $2.5 billion Mariner East 2 propane and natural gas liquids pipeline in Pennsylvania. Residential building in March registered moderate growth, helped by a rebound for multifamily housing after a subdued February. Nonresidential building in March held steady with its February pace, as strong activity for office buildings and airport terminals offset a steep drop for manufacturing plants. Through the first three months of 2017, total construction starts on an unadjusted basis were $160.1 billion, down 3% from the same period a year ago (which included heightened activity for manufacturing plants and electric utilities/gas plants). If the often volatile manufacturing plant and electric utility/gas plant categories are excluded, total construction starts during the first three months of 2017 would be up 8% relative to last year.

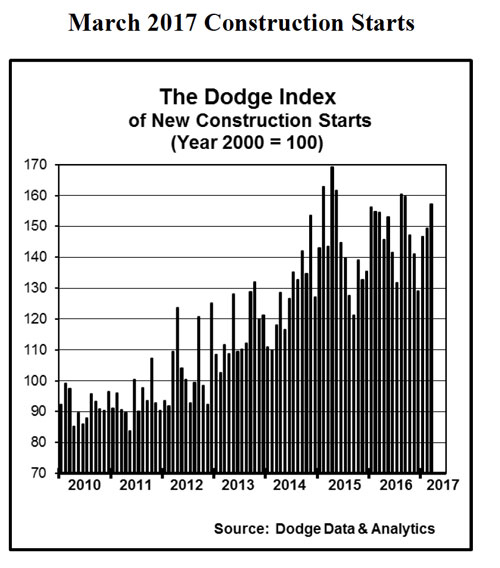

The March data produced a reading of 157 for the Dodge Index (2000=100), compared to 149 in February and 147 in January. After sliding to a weak 129 in December, the Dodge Index over the next three months bounced back 22%. On a quarterly basis, the Dodge Index averaged 151 during this year’s January-March period, up 9% compared to the 139 average for the fourth quarter of 2016.

“The pattern for construction starts in early 2017, with three straight monthly gains, is the reverse of the three straight monthly declines that closed out 2016,” said Robert A. Murray, chief economist for Dodge Data & Analytics.

“While the construction start statistics will frequently show an up-and-down pattern, whether month-to-month or quarter-to-quarter, the improved activity in this year’s first quarter provides evidence that the construction expansion is still proceeding,” Murray said.

“This year’s first quarter has seen nonresidential building and public works rebound from the loss of momentum each experienced towards the end of 2016, helped respectively by the strong activity so far in 2017 for new airport terminal projects and new pipeline projects. Nonresidential building in 2017 should be able to stay on its upward track, supported by further growth for such institutional project types as school construction. As for public works, it’s also expected to show improvement over the course of 2017, although its prospects are less certain given its connection to legislative developments at the federal level. This includes how Congress will deal with the continuing resolution for fiscal 2017 appropriations scheduled to expire at the end of April, and whether a new federal infrastructure program will get passed this year.”